Cashflow & Rental Yield in 2026: What Investors Need to Watch

Cashflow is one of the most misunderstood concepts in property investing in 2026. Stop assuming that a high rental yield automatically means strong cashflow.

Rising holding costs, tighter lending buffers, and uneven rent growth mean that positive cashflow is harder to achieve and easier to miscalculate than it was a decade ago. A property can show a 6% gross yield and still quietly drain your bank account once realistic expenses and financing are applied.

If you are prioritising rental income, or you are cautious about over-leveraging and protecting capital, the goal is not to chase the highest yield. The goal is to acquire a property that delivers consistent, stress-tested net cashflow after real costs. Here is how rental yield actually works in 2026, and how to evaluate it properly.

What Cashflow Property Investing Means in 2026

Cashflow investing today is not about buying a “high-yield” property and expecting surplus income to appear. It means evaluating net performance after realistic ownership costs.

True cashflow considers:

Actual rent achieved, not just advertised estimates

Vacancy and tenant turnover

Interest rates above today’s rate

Ongoing ownership costs that increase over time

If you are focused on income, what matters is what remains after everything is paid. Not what the marketing brochure promises.

Rental Yield Explained Properly

Before assessing cashflow, you need clarity on rental yield.

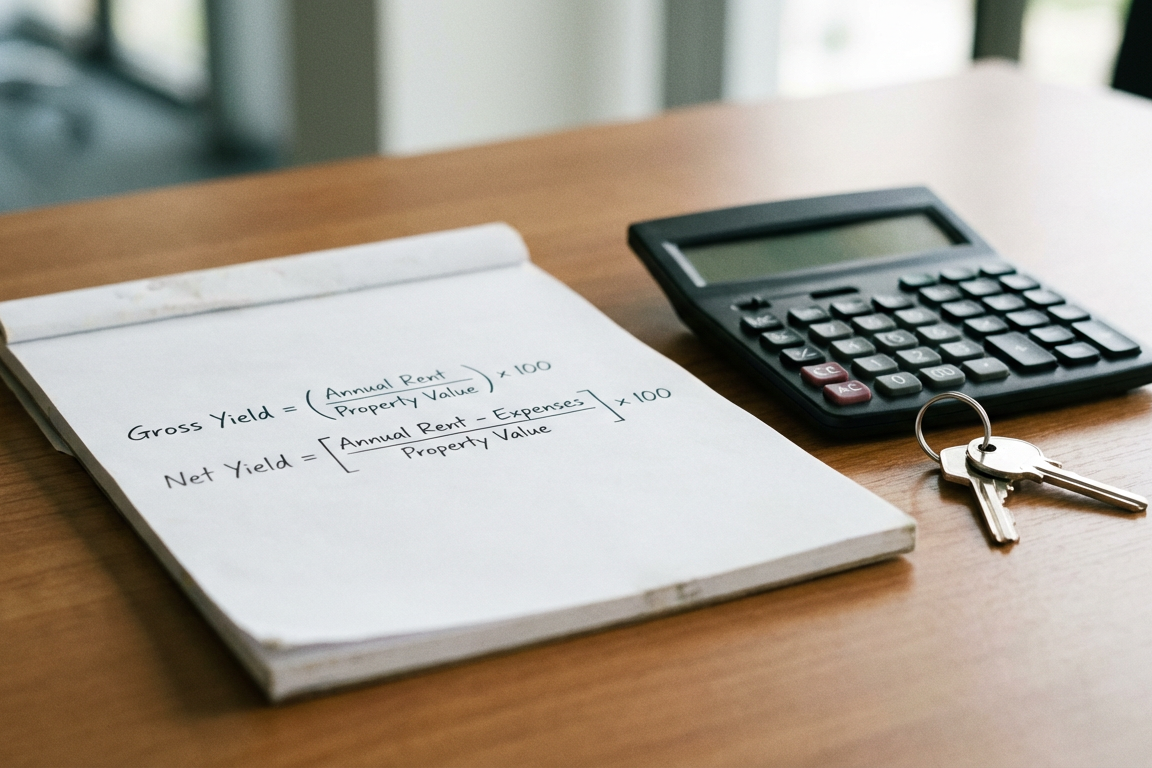

Gross Yield

Gross yield is calculated as:

Annual rent ÷ Purchase price

Example:

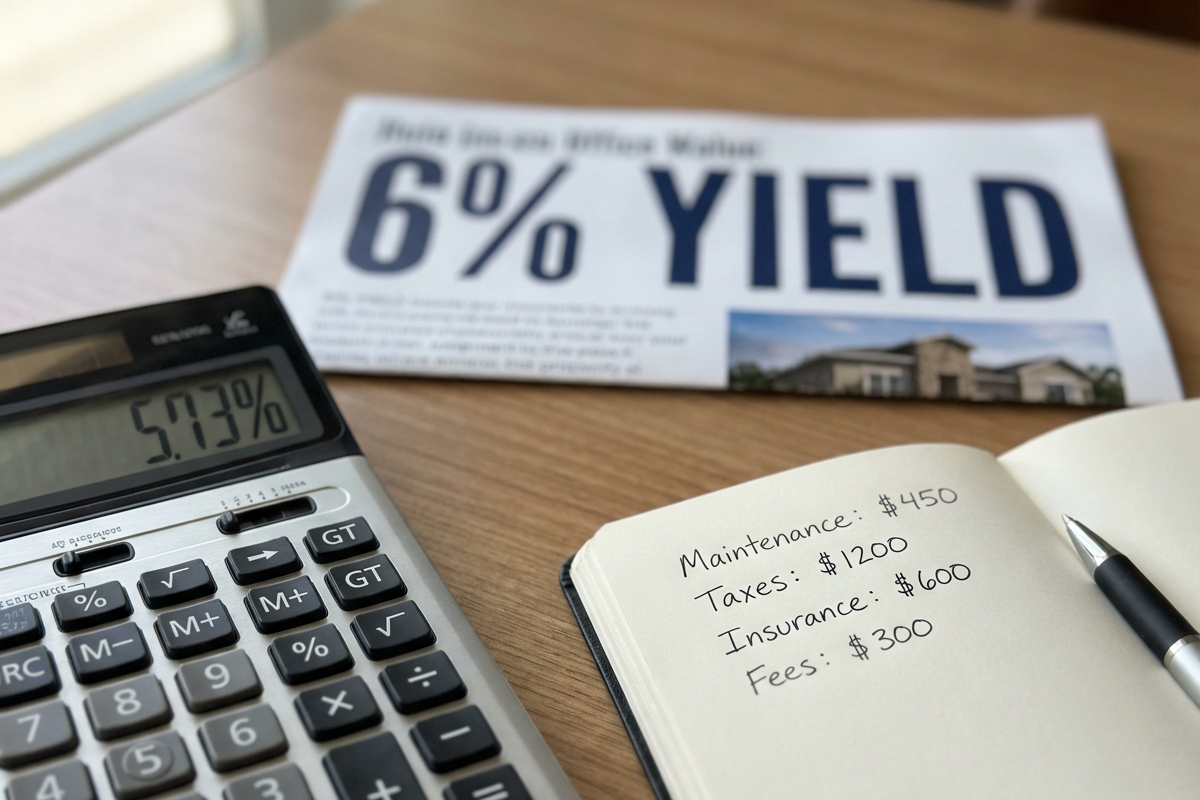

$28,000 annual rent ÷ $500,000 purchase price = 5.6% gross yield.

Gross yield is easy to calculate. It is also incomplete.

Net Yield

Net yield accounts for real expenses:

Annual rent minus:

Property management fees

Insurance

Council rates

Maintenance

Land tax if applicable

Then divided by purchase price. Using the same example:

$28,000 rent minus $9,000 annual expenses ÷ $500,000 = 3.8% net yield.

In 2026, net yield is what matters. A property advertised at 6% gross may deliver only 3% to 4% net once real costs are included. If you are prioritising stable rental income, gross yield alone is not enough.

Why Yield Alone Does Not Equal Cashflow

Even net yield does not fully determine cashflow.

Cashflow depends on:

Loan structure and leverage

Interest rate assumptions

Tax position

Unexpected repairs

Vacancy variability

The same property with 5% net yield can produce very different outcomes at 70% LVR versus 90% LVR.

Higher leverage does not improve cashflow. It increases pressure. If your objective is reliable income, financing must be modelled as carefully as rent.

The Real Costs Investors Must Factor In

Most cashflow miscalculations come from optimistic cost assumptions.

In 2026, you must realistically include:

Property management at 8% to 10% of gross rent

Letting fees

Insurance and council rates increasing 3% to 4% annually

Maintenance allowance of 1% to 1.5% of property value

Land tax exposure where relevant

Interest rates modelled at 6.5% to 7%, not just current rates

If your projections look attractive only because you minimised these assumptions, the property is not robust. Conservative modelling is not pessimism. It is protection.

The 3 Checks That Protect You From Cashflow Traps

If you want to avoid buying a property that looks good on paper but drains cash in reality, apply these three checks.

1. Model rent below appraisal

If rent is appraised at $450 per week, model it at $400 to $410. Budget at least 4 to 6 weeks of vacancy annually. If the property still produces positive net cashflow under that assumption, you have margin. If it only works at top-of-range rent with zero vacancy, it is fragile.

2. Model interest above current rates

If your loan is at 5.5%, model at 6.5 to 7%. Interest rates change. Serviceability buffers tighten. If you can comfortably hold at higher rates, your position is defensible. If you rely on today’s rate to make the numbers work, you are exposed.

3. Stress-test maintenance and liquidity

Older properties can show higher yield but heavier maintenance variability. Newer properties may show lower yield but more predictable costs.

Ask yourself:

Can I handle a major repair without stress

If vacancy extends to 8 weeks, can I hold

If I need to exit, is there sufficient buyer demand

A property that survives stress scenarios protects your capital.

How Cashflow Behaves Across Property Types

Not all properties deliver income the same way.

Lower-priced properties:

Often show 6% to 7% gross yield

May carry higher maintenance and vacancy risk

Newer properties:

Often show 4% to 5% gross yield

Typically deliver more predictable holding costs

Regional properties:

May show 5% to 7% yield

Can carry liquidity risk and narrower tenant pools

Established metro properties:

Often yield 4% to 5%

Offer stronger tenant diversity and resale demand

If you are focused on stable income, consistency often outperforms chasing the highest percentage.

Common Cashflow Mistakes in 2026

Investors frequently:

Rely on best-case rent

Ignore vacancy assumptions

Underestimate maintenance

Confuse tax deductions with real cash

Over-leverage barely positive properties

Tax deductions improve overall returns. They do not create cash in your account. Leverage amplifies both gains and stress. High Yield Often Looks Safer Than It Really Is walks through how these mistakes show up in real deals and why strong rent figures can mask weak fundamentals.

Should You Prioritise Cashflow Over Growth?

This depends on your holding capacity and risk tolerance. If your priority is income stability and protection, cashflow must come first. If you can comfortably sustain neutral or mildly negative cashflow, growth-focused assets may complement your strategy.

Most disciplined investors aim for balance:

At least neutral to mildly positive net cashflow

Sustainable tenant demand

Growth supported by fundamentals

The mistake is chasing growth while ignoring income stress. If you are still working out that balance, cash flow vs capital growth property lays out how each approach builds wealth over time and why most investors end up blending the two.

Stress-Test Before You Acquire

Before committing, model three scenarios.

Best case:

Rent at top appraisal

Minimal vacancy

Current interest rate

Realistic case:

Rent 10% below appraisal

4 to 6 weeks vacancy

Interest rate 0.5% higher

Stress case:

Rent 15% to 20% below appraisal

8 to 10 weeks vacancy

Interest rate 1.5% higher

If you can comfortably hold in the stress case, you are buying defensively. If you cannot, you are relying on optimism. How To Assess A Property Deal In 2026 builds on this stress‑testing approach and shows you how to combine yield, demand and supply checks before you call any property a “cashflow deal”.

Conclusion

Cashflow property investing in 2026 requires discipline. Stop assuming yield equals income.

Focus on:

Net performance after real costs

Conservative rent modelling

Interest rate buffers

Stress-tested holding capacity

The investors who build stable portfolios are not the ones chasing the highest headline yield. They are the ones acquiring properties that still work when conditions tighten.

If you want clarity on whether a property genuinely delivers net cashflow under conservative modelling, the next step is aligning suburb selection, financing structure, and income tolerance with your broader strategy.